Banking is becoming a battle of two competing narratives. On one side are the banks themselves, their CEOs giving their quarterly pep talks to shareholders, claiming to actually run the banks. On the other side are the central banks, using those same banks as a channel to carry out their policy decisions at the same time as regulating their activities.

As quantitative easing has expanded beyond its already dizzying levels during the pandemic, the link to central banks becomes stronger and stronger. And the conflict between QE and regulation is growing.

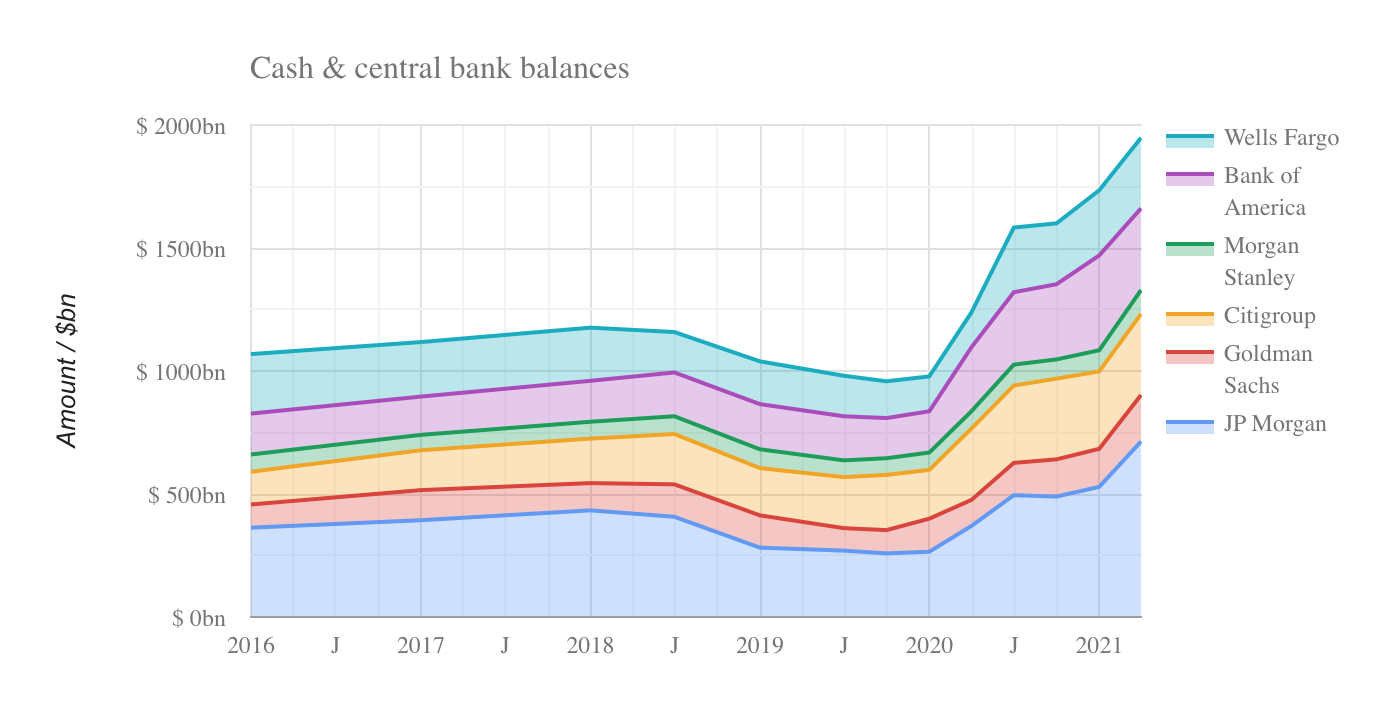

Start by reviewing some balance sheet figures. The asset side of the Federal Reserve balance sheet has grown by $3.5 trillion since the start of the pandemic in March 2020, as a result of bond buying. The Fed funded these QE assets on the liability side by crediting banks that sold the bonds with additional reserves.

According to Fed data, these reserves increased by $2 trillion since March 2020, and the Risky Finance banking tool shows that $1 trillion of this increase was concentrated at the six largest banks. Putting it another way, excess reserves now account for ten per cent of their balance sheet assets.

Now these large banks have simultaneously seen their customers react to the pandemic, such as by increasing deposits, while making their own investment decisions, such as buying securities. But now, the ballooning central bank deposits are starting to crowd out this activity.

UK motor finance scandal reawakens ghost of PPI

UK motor finance scandal reawakens ghost of PPI

Smoke, mirrors and net interest margins

Smoke, mirrors and net interest margins

The self-fulfilling prophecy of public sector pensions

The self-fulfilling prophecy of public sector pensions

HSBC’s overvalued Chinese bank

HSBC’s overvalued Chinese bank